What Is FIFO? How It Works in Retail & eCommerce

Think about the milk section at any grocery store. The staff places newer bottles at the back and older ones up front. Customers grab from the front and nothing expires on the shelf. That is FIFO in physical form. In accounting and inventory management, this same logic gets formalized and it has real consequences for your profit margins, tax obligations, and balance sheet.

In this blog, we will learn what is FIFO, how it works with a real example, where it applies across industries, how it compares to LIFO and Weighted Average, and when it may or may not be the right fit for your business.

TL;DR

- FIFO stands for First In, First Out. It is the oldest inventory is sold or expensed first

- It works as both a physical warehouse practice and an accounting cost-flow method

- Under FIFO, older costs hit COGS first which results in higher reported profit during inflation

- It is accepted under both IFRS and GAAP and is the dominant global method since IAS 2 prohibits LIFO, leaving FIFO and Weighted Average as the two permitted options

- Best suited for businesses with perishable goods, seasonal stock, or expiry-sensitive products

- Compared to LIFO, FIFO better reflects current inventory value on the balance sheet

- A third option, the Weighted Average method, blends all purchase costs into one average and is useful for stable-price, high-volume businesses

What Is FIFO?

FIFO stands for First In, First Out. It is an inventory management and accounting method where the oldest stock is sold, used, or expensed before newer stock. The first item that enters your inventory is the first item that leaves.

In accounting, the cost of your earliest purchased inventory is assigned to the Cost of Goods Sold (COGS) first. In a warehouse, it means the oldest unit on the shelf gets picked before the one behind it. According to survey data, approximately 55% of companies use FIFO as their primary inventory valuation method.

Under IAS 2; the international standard governing inventory accounting; LIFO is explicitly prohibited. FIFO and Weighted Average are the two permitted cost formulas. Because LIFO is banned across most of the world,

FIFO has become the dominant choice for internationally reporting companies. As of May 2025, the IFRS Foundation reports that IFRS standards are required in 169 jurisdictions worldwide.

How Does FIFO Work?

The core COGS formula is unchanged:

COGS = Starting Inventory + Purchases − Ending Inventory.

What FIFO changes is which costs get assigned to sold units first.

Here is a clean, practical example:

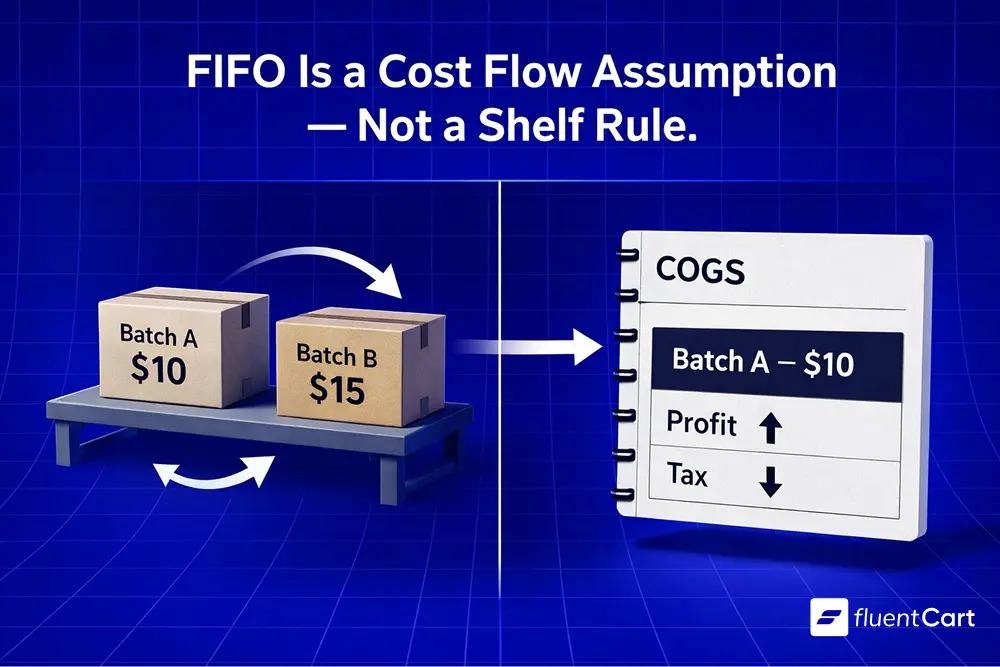

A store buys 100 units in January at $10 each, then another 100 units in March at $15 each. In April, they sell 120 units.

Under FIFO:

- First 100 units sold at $10 each (January batch, oldest first)

- Next 20 units sold at $15 each (March batch)

- Total COGS = $1,000 + $300 = $1,300

- Remaining inventory = 80 units valued at $15 each (the newer stock)

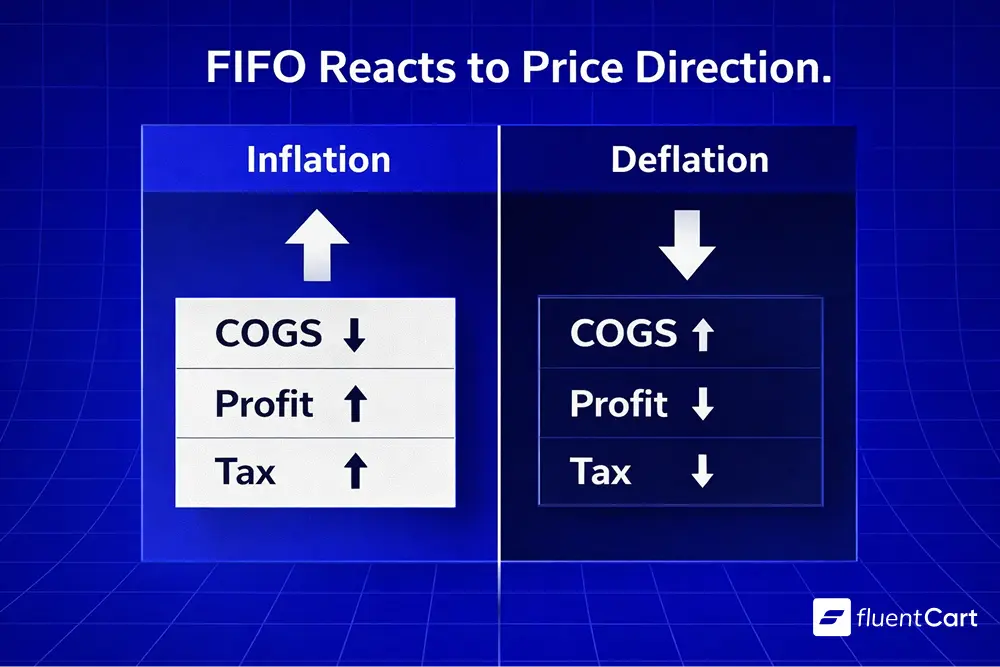

FIFO keeps the most recent purchase costs on your balance sheet as ending inventory value. During inflation, when new stock tends to cost more, your reported inventory asset stays closer to what replacement stock would actually cost today.

For businesses that present financials to investors or lenders, FIFO-based statements tend to show higher inventory asset values and higher reported profit during inflation. Financial analysts also commonly restate LIFO-based financials to a FIFO basis for cross-border comparison, a practice noted in KPMG’s IFRS vs US GAAP inventory guidance.

One important clarification: you do not have to physically sell the oldest unit first to use FIFO in accounting. It is a cost-flow assumption. You apply it to how costs move through your books regardless of which physical unit left the shelf.

FIFO in Inventory Management vs. Accounting

FIFO operates in two distinct contexts and conflating them causes real confusion for new learners.

1. Physical Inventory Management

FIFO means organizing your stock so older products are stored at the front and picked first. A grocery store that stacks fresh dairy behind last week’s batch is doing this. A warehouse that picks the earliest-received carton before a newer one is doing this too. The goal is to prevent spoilage, expiry, or obsolescence from quietly eating into your margins.

2. Accounting

FIFO is a cost-flow assumption. You calculate COGS as if the oldest units sold first, even if the actual physical movement was mixed. This affects your income statement through COGS and your balance sheet through ending inventory value. Both applications serve the same business interest: making sure old stock does not pile up unnoticed on your shelves or in your financial records.

If you manage ecommerce fulfillment, understanding this distinction matters. Your warehouse team and your accountant can both be “using FIFO” and mean two completely different things.

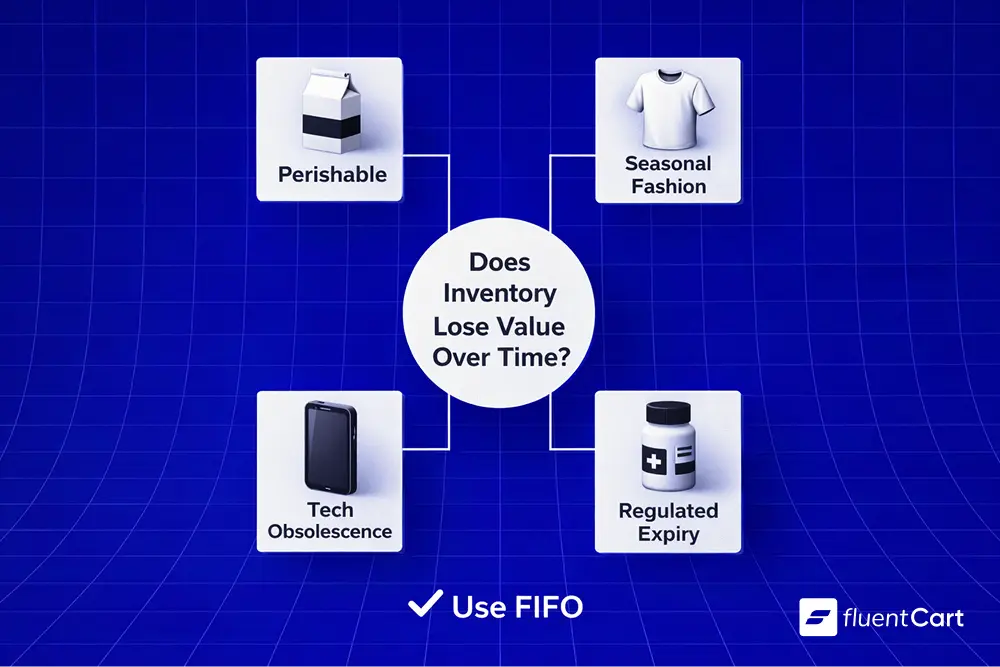

Industries That Rely on FIFO

FIFO is not industry-specific but some sectors depend on it more than others.

- Food and grocery retailers apply it by necessity. New stock goes to the back and older stock faces the customer. Expired product on shelves is both a health risk and a direct write-off.

- Pharmaceuticals operate under FDA cGMP regulations (specifically 21 CFR Part 211) and EU GDP Guidelines which mandate stock rotation. In practice, most pharmaceutical warehouses use FEFO (First Expired, First Out) over pure FIFO as they prioritize expiry date over receipt date.

- For raw materials and packaging without expiry concerns, FIFO still applies. The principle in both cases is the same: older or sooner-to-expire stock leaves first.

- Fashion and apparel brands treat trend cycles the way food businesses treat expiration dates. A summer dress bought in January needs to move before the next collection arrives or it becomes deadstock.

- Electronics face rapid obsolescence. Last year’s chip or smartphone model depreciates fast once newer SKUs hit the market, so the first batch in must be the first batch out to protect margins.

Any business where inventory loses value over time benefits directly from FIFO discipline.

Benefits of Using FIFO

FIFO’s advantages go beyond compliance. Some of its benefits include:

- Reduces spoilage and obsolescence risk: By keeping inventory moving in chronological order, products spend less time sitting idle. Less idle inventory means fewer write-offs and lower holding costs.

- Gives a more accurate balance sheet: Since the remaining unsold inventory carries the most recent purchase costs, the ending inventory value better reflects what replacement stock would actually cost today.

- Easier to implement and audit: FIFO follows the natural flow of most businesses so explaining your cost logic to an auditor or accountant is straightforward. Most ecommerce accounting and inventory software supports FIFO by default with minimal customization required.

- During inflation, FIFO also produces higher reported gross profit since the cheaper, older inventory hits COGS first. This can strengthen the financial picture presented to investors and lenders.

Note: The trade-off is that higher reported profit also means higher taxable income. A real cost worth planning for.

FIFO vs. LIFO vs. Weighted Average

Three methods dominate inventory valuation. Each produces different COGS, different profit figures, and different tax outcomes from the same underlying transactions.

| Factor | FIFO | LIFO | Weighted Average |

| Cost assignment | Oldest first | Newest first | Blended average of all units |

| COGS during inflation | Lower | Higher | Middle ground |

| Reported profit | Higher | Lower | Moderate |

| Ending inventory value | Reflects current costs | Understated | Averaged |

| Global acceptance | Permitted under IFRS and GAAP | US only under GAAP; prohibited under IAS 2 | Permitted globally |

| Best for | Perishables, fast-moving goods | Non-perishables, inflation tax strategy | High-volume, stable-price products |

Weighted Average works by dividing the total cost of all available inventory by the total number of units and then applying that single average cost to every sale. It smooths out price spikes and is simpler to automate at scale.

For ecommerce businesses with large SKU counts and relatively stable purchase prices, it is often the operationally easiest path. FIFO remains the natural default for any business where stock rotation by age actually matters.

Challenges of FIFO You Should Know

No method is without trade-offs and FIFO is no exception.

The most discussed drawback is its tax exposure during inflation. Because FIFO expenses the cheapest (oldest) inventory first, your gross profit looks higher. Higher profit means higher income tax. Businesses that prioritize tax minimization over financial presentation should study LIFO as the US-only alternative worth understanding.

For businesses with

- large,

- diverse,

- or high-volume inventories,

Maintaining strict FIFO records layer by layer can get complex without dedicated software. Manual tracking of purchase dates and batch costs is prone to errors at scale. A solid ecommerce management system handles cost assignment automatically so your team does not have to chase it manually.

Finally, in industries with rapid product evolution, the oldest inventory can sometimes become outdated before FIFO fully cycles it out. This creates a mismatch between the accounting assumption and physical reality; one worth monitoring in fast-moving product categories.

Wrapping Up

FIFO is not just an accounting method. It is a way of running a cleaner, more accountable business. For most retail and ecommerce businesses that deal with physical goods, perishables, or seasonally sensitive stock, FIFO is both the natural and globally dominant choice. It keeps your shelves honest, your books accurate, and your balance sheet credible.

The discipline is simple: sell old before new and account for it the same way. Once that becomes habit in your warehouse and your accounting system, everything else becomes easier to manage.

Once In a Lifetime Offer

Frequently Asked Questions

Does FIFO affect how I physically store and ship products, or is it purely an accounting rule?

Both. In accounting, FIFO is a cost-flow assumption. You record costs as if the oldest units sold first regardless of what physically left the shelf. In warehouse and fulfillment operations, FIFO is also a physical practice where older stock is stored at the front and picked first. This prevents spoilage and product obsolescence in day-to-day operations.

Is FIFO legally required in any industry or country?

Under IAS 2, LIFO is prohibited and FIFO is one of two permitted cost formulas alongside Weighted Average. IFRS is required in 169 jurisdictions as of May 2025, per the IFRS Foundation. In the US, FIFO is accepted under GAAP alongside LIFO. In pharmaceuticals, FDA regulations under 21 CFR Part 211 mandate adequate stock rotation controls with FEFO being the practical standard for products that carry expiry dates.

Can a small ecommerce business benefit from FIFO, or is it mainly for large retailers?

FIFO scales to any business size. A small online store selling handmade goods benefits just as much as a large distributor. It prevents older raw materials from sitting idle, keeps product quality consistent, and aligns naturally with how most small businesses already move inventory. It also simplifies bookkeeping since the cost flow matches real operational behavior and makes it easier to manage without a dedicated accounting team.

How does FIFO behave during deflation (falling prices)?

When prices fall, FIFO works against your tax position. Older inventory was purchased at higher prices. Expensing it first against sales at current lower prices raises your reported COGS, which reduces reported profit and lowers taxable income. Your balance sheet also shows ending inventory at the newer, lower cost which can make asset values appear weaker. In deflationary environments, FIFO can make a business look less profitable than it actually is in cash terms.

Deputy Marketing Lead, published literary author, and musician. I thrive on marketing for tech companies while composing music, collecting books of lasting depth, exploring cinema with a discerning eye, and studying the arts and history.

Subscribe now

Related Articles and Topics

-

What I Ask My Store Every Morning (Before My Coffee Gets Cold)

Hi, I’m Jewel, founder of WPManageNinja. We build FluentCart, FluentCRM, and the rest of the Fluent plugins. I…

-

What Is a Trade Show? Meaning, Types, and Purpose Explained

A trade show is where businesses display products to industry buyers. See its meaning, types, and purpose explained.

-

What Is a Fixed Cost? Definition, Examples, and Formula

Learn what a fixed cost is, how it differs from variable cost, real examples, and the formula to…

Leave a Reply