eCommerce Business Insurance (2026) [Guide]

Selling online carries real legal and financial risk from the first transaction. Product injuries, data breaches, inventory loss, and supplier failures are all possibilities that personal insurance policies will not cover.

eCommerce business insurance exists to fill that gap. In this blog, we will walk through what eCommerce insurance covers, how much it costs, and how to choose the right policies for how your store operates.

TL;DR

- eCommerce business insurance protects online stores from product liability claims, data breaches, inventory loss, and lawsuits

- Core coverage types: general liability, product liability, cyber liability, commercial property, and business interruption

- Dropshippers, inventory holders, and digital sellers each face different risks and need different coverage

- Some sales channels, like Amazon, require proof of insurance once you cross certain revenue thresholds

- Standard homeowner’s policies do not cover business activity

What Is eCommerce Business Insurance?

eCommerce business insurance is a category of commercial policies designed to protect online retailers from financial losses tied to their business operations. It covers

- liability claims,

- property damage,

- data breaches,

- and legal costs that fall outside what personal or standard homeowner’s policies protect.

The core reason eCommerce needs its own coverage is that it combines physical and digital risk in a single operation. A sold product can injure a customer.

Stored payment data can be compromised. Warehouse inventory can be destroyed in a fire. Each scenario carries real exposure, and a single uncovered incident can cost more than years of premiums combined.

Key Risks Online Sellers Face

Knowing where your store is exposed makes coverage decisions much easier.

- Product liability: Even when dropshipping or reselling, you can be held legally responsible if a product causes injury or property damage. Liability extends to every business in the supply chain, not just the manufacturer.

- Cyber threats: Online stores collect payment details, email addresses, and order histories. Data breaches cost an average of $4.4 million to resolve, with AI-powered attacks now among the top threats. A breach can also trigger customer notification requirements and regulatory fines across every state where affected customers live.

- Inventory loss: Stock destroyed by fire, flood, or theft is an uninsured loss without commercial property coverage. Standard homeowner’s policies typically exclude business inventory kept at home.

- Business interruption: A supplier failure, platform outage, or warehouse incident can halt revenue while fixed costs continue. Without coverage, that gap comes entirely from your operating budget.

- Payment fraud and chargebacks: Fraudulent orders reverse into chargeback fees. High chargeback rates can result in payment processor penalties or account suspension.

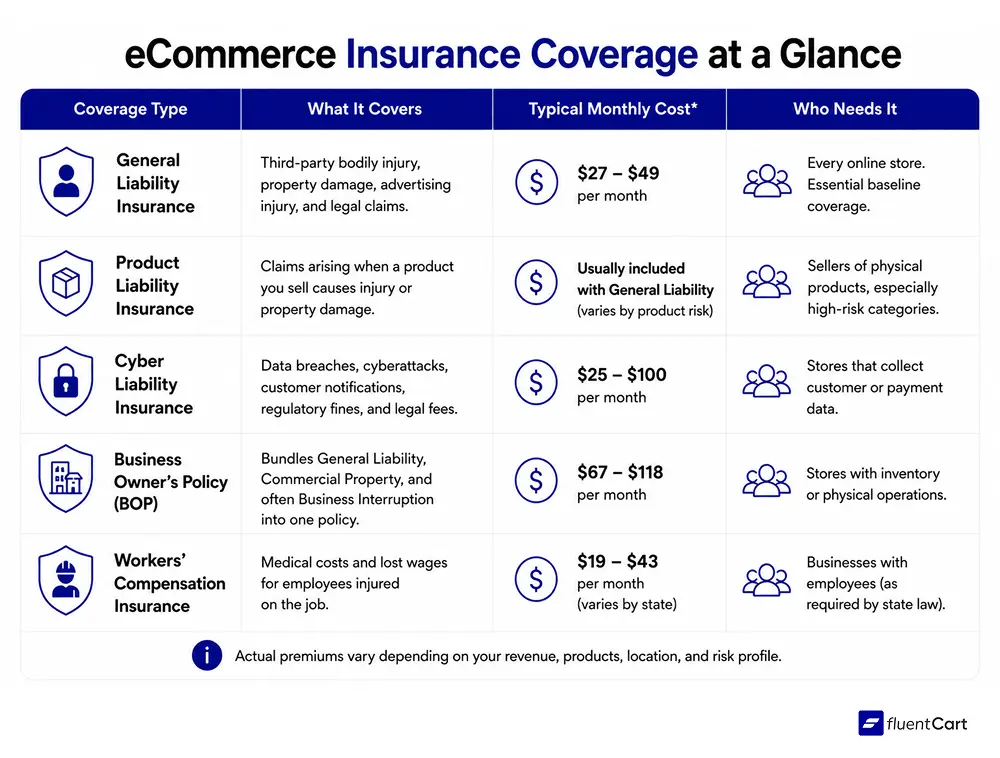

6 Types of eCommerce Insurance Coverage

No single insurance policy covers every risk. Most online businesses need a combination of coverages based on how they operate. Here are the 6 types of eCommerce insurance coverage that you should know about.

1. General Liability

General liability (GL) insurance covers third-party claims for bodily injury, property damage, and advertising injury. It is the baseline coverage nearly every eCommerce business needs.

Amazon requires $1 million per occurrence general liability once sellers reach $10,000 in monthly sales, with Amazon named as an additional insured. Walmart has similar requirements.

2. Product Liability

Product liability covers claims that a product you sold caused injury or property damage, whether you manufactured it or not. It is critical for sellers of supplements, electronics, children’s products, and imported goods.

For most policies, product liability is included within general liability. Verify the limits before assuming your category is adequately covered.

3. Cyber Liability

Cyber liability covers costs from a data breach or cyberattack: customer notification, legal fees, and regulatory fines. Standard general liability and business owner’s policies do not cover cyber incidents.

A small store with 5,000 customer records at risk can face remediation costs between $60,000 and $120,000. A standalone cyber policy runs $25 to $100 per month for $1 million in coverage.

4. Commercial Property Insurance

Commercial property insurance covers physical assets such as inventory and equipment against fire, theft, and flooding. Home-based sellers cannot rely on homeowner’s coverage for business stock.

Merchants using third-party fulfillment centers should also verify that their own policy covers off-site inventory, since the center’s policy covers its facility operations, not your goods.

5. Business Interruption Insurance

Business interruption insurance replaces lost income when a covered event halts operations. Coverage for supplier failures or platform outages depends on specific policy language.

This coverage is often bundled into a Business Owner’s Policy (BOP) alongside general liability and commercial property, which tends to be more cost-effective than purchasing each separately.

6. Workers’ Compensation

Workers’ compensation covers medical costs and lost wages for employees injured on the job. Most US states require it for any business with employees. Sellers with warehouse staff or in-house fulfillment teams should confirm state requirements with a licensed insurance professional.

Coverage by Business Model

Different eCommerce business models face different risks, so the right insurance coverage depends on how your store operates.

Dropshippers and Print-on-Demand Sellers

Dropshippers do not hold inventory but remain exposed to product liability as the seller of record. Cyber liability still applies because customer data is collected regardless of the fulfillment method. Supplier agreements are worth reviewing carefully. A manufacturer’s liability policy covers its own operations, not yours.

A small business thread on Reddit confirmed that most eCommerce sellers need general liability, product liability, and cyber liability as their core stack.

Inventory-Holding Merchants

Merchants holding stock need commercial property coverage on top of general liability and product liability. A BOP typically makes the most practical sense here.

Home-based sellers with on-site inventory need a standalone commercial policy since standard homeowner’s coverage does not substitute.

Digital Product Sellers

Digital product sellers have limited exposure to product liability and commercial property risk. Their primary concerns are cyber liability and professional liability, also called errors and omissions insurance.

If a customer claims a digital product failed to deliver as described, professional liability covers that claim.

How Much Does eCommerce Insurance Cost?

eCommerce business insurance costs range from $227 to $1,457 annually on average. The final figure depends on coverage type, state, and product category. A full bundled policy that combines a BOP with workers’ compensation and professional liability averages $188 per month.

Typical monthly ranges for individual coverage types:

- General liability: $27 to $49 per month

- Business owner’s policy (BOP): $67 to $118 per month

- Cyber liability: $25 to $100 per month

- Workers’ compensation: $19 to $43 per month, varies by state

Premiums rise with product risk category, revenue, volume of customer data stored, international sales activity, and prior claims history. A licensed insurance professional can quote based on your actual profile.

When to Get Covered

- Before your first sale: Liability applies from the first transaction. Home-based sellers with inventory on-site need coverage before launch.

- At your first hire: Workers’ compensation requirements trigger in most states at this point. Employment practices liability also becomes relevant.

- When inventory or revenue grows: A basic policy may not keep pace with expanded stock or new product categories. Review coverage when your business materially changes.

How to Choose a Provider

Not all small business policies are built with eCommerce in mind. Before committing, confirm these points:

- Products covered: Some product categories may be excluded based on risk profile. Verify your catalog is covered.

- Sales channels: A policy for one storefront may not extend to Amazon, Etsy, or social commerce sales.

- International sales: Confirm whether product liability and cyber coverage applies to claims outside your home country. GDPR adds data protection obligations that many domestic policies do not address.

- Cyber policy scope: A BOP cyber endorsement often sublimits coverage significantly compared to a standalone cyber policy. Confirm what breach costs are actually covered.

- Third-party storage: Verify that inventory stored at a fulfillment center or third-party logistics provider is explicitly covered under your own policy.

Compare rates and terms across at least two or three providers before committing.

Wrapping Up

eCommerce business insurance is not a luxury once your store is generating revenue. The risks are real and the premiums for solid core coverage are lower than most sellers expect.

Start with general liability, product liability, and cyber liability. Add commercial property if you hold inventory and business interruption if revenue disruption is a real operational risk. Review coverage whenever your business structure, product range, or sales channels change.

How your store handles data ownership and eCommerce management matters too. Clear systems on both fronts, built before an issue arises, are worth the effort as you scale.

FAQs

Do dropshippers need eCommerce business insurance?

Yes. Dropshippers are the seller of record, so product liability can extend to them even when a supplier handled the product. Cyber liability also applies because customer data passes through their store.

Does a homeowner’s policy cover a home-based eCommerce business?

Generally no. Standard homeowner’s policies exclude business activity and will not cover inventory stored at home for business use. A standalone commercial policy or business endorsement is required.

What insurance does Amazon require from sellers?

Amazon requires $1 million per occurrence general liability coverage with Amazon listed as an additional insured, triggered once a seller reaches $10,000 in monthly sales.

Deputy Marketing Lead, published literary author, and musician. I thrive on marketing for tech companies while composing music, collecting books of lasting depth, exploring cinema with a discerning eye, and studying the arts and history.

Subscribe now

Related Articles and Topics

-

eCommerce Data Ownership: Why Your Customer Records Decide Who Survives 2026

Your store does not own its customers. Right now, today, in June 2026. And the platforms hosting your…

-

What is a Patent? Definition, Business Use Cases, and how to apply

A patent grants inventors exclusive rights to their invention for up to 20 years. Learn the meaning, types,…

-

How Much Is My Business Worth? Business Valuation

Learn how to value your business using SDE, EBITDA, and market comparables. Practical methods to calculate what your…

Leave a Reply